From the Financial Crisis in 2008 up to the beginning of the COVID-19 pandemic, foreign stocks failed to keep pace with U.S. stocks, and the margin was wide. Between April 2009 and December 2019, the MSCI USA Index outperformed the MSCI ACWI ex USA Index by about 7 percentage points annually.

There are several factors that can be looked at to explain the divergence. First, technology stocks have been among the best performers of the past decade and represent a larger share of the U.S. market than foreign markets. Additionally, the appreciating U.S. dollar hurt foreign stocks’ dollar-denominated returns. While U.S. markets have benefitted from both trends, deeper analysis reveals that differences in sector composition and a strong dollar played a relatively small role. Differences in earnings growth and stock selection explain most of this gap.

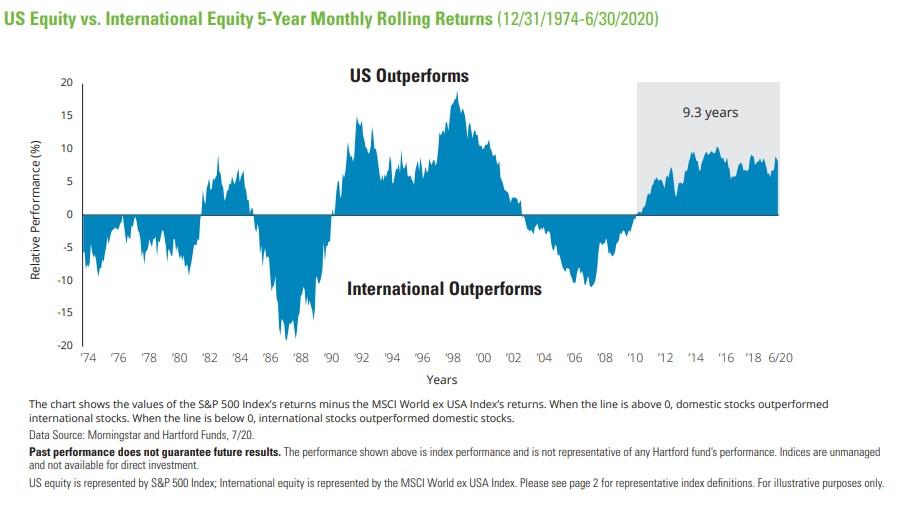

While U.S. stocks outperformed foreign stocks in the period following the financial crisis, this hasn’t always been the case. Historically, these markets have taken turns outperforming each other. Investing in both makes sense because it is difficult to determine which one will outperform in the future. While over the past decade U.S. stocks have outperformed foreign stocks, we know that a market cannot move in one direction forever. The question isn’t “will foreign stocks come back?” it is a matter of when. The chart below demonstrates the cycle of outperformance.

Identifying stock selection and earnings growth as the primary contributing factors of why U.S. stocks have outperformed foreign stocks over the past decade makes the case for active management in international equities. International investing is significantly more complicated than domestic investing, with a combination of political, liquidity, and currency risks. These factors can create more inefficiencies within individual stocks than domestic markets. Active managers can maneuver a portfolio to take advantage of these inefficiencies by hedging these risks in order to reduce a portfolio’s overall risks and enhance its risk-adjusted return. For example, suppose that an investor has a choice between a country ETF that invests broadly across asset classes or an actively managed fund focused on that country. A fund manager may notice that politicians in the country are seeking to nationalize energy industry assets and decide to sell off those assets to mitigate risks. By comparison, an index fund would be forced to continue holding those assets and risk the nationalization destroying value. Active managers with local knowledge can help predict these kinds of risks better than the average investor.

Studies have shown that equity markets that provide a larger number of independent investment opportunities are richer for active managers. International large-caps, global small-caps, and emerging markets offer a much more diverse stock selection universe: a larger number of securities from multiple countries of listing with varied currency denominations. Studies have also shown that in these sectors, active managers have added incrementally higher value for several years following the Global Financial Crisis. The trend that U.S. investments can’t outperform foreign investments and the case for active management in international markets suggest that despite the underperformance over the past decade, there is a case for investing in actively managed international funds for the future.

The main risks of international investing are currency fluctuations, differences in accounting methods; foreign taxation; economic, political or financial instability; lack of timely or reliable information; or unfavorable political or legal developments. This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact a financial professional for more information specific to your situation.

By Elizabeth Schleifer, CFP®