When the 2017 Tax Cuts and Jobs Act was passed, articles were being released everyday covering the new tax brackets, eliminated itemized deductions, and more. What received less attention was the Federal Qualified Opportunity Zone Program it introduced, which offers some especially unique tax benefits for those who are willing to invest in certain low-income areas designated as “Qualified Opportunity Zones.”

The Opportunity Zone program was created to revitalize economically distressed communities using private investments rather than taxpayer dollars. To stimulate participation in the program, taxpayers who invest in Qualified Opportunity Zones are offered capital gains tax incentives available exclusively through the program. Each state nominates blocks of low-income areas, which are then certified by the Secretary of the U.S. Treasury.

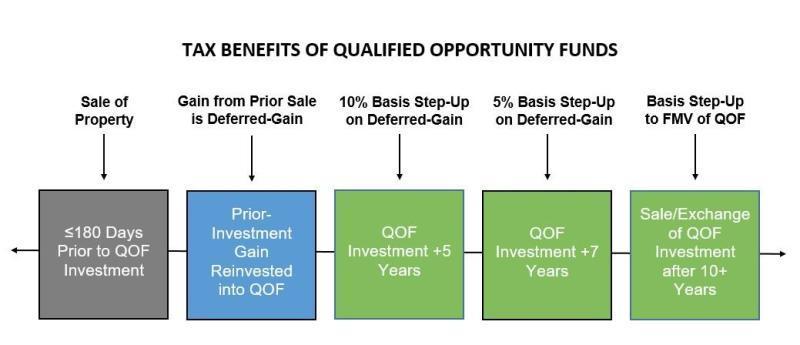

The actual vehicles for investment into Opportunity Zones are called Qualified Opportunity Funds (QOF). These vehicles are structured as either partnerships or corporations for federal tax purposes. The fund is required to hold at least 90% of its assets in “qualified opportunity zone property,” which can be stock, partnership interest, or business property.

The benefit comes into play when a taxpayer sells an asset and generates a capital gain. The taxpayer then has 180 days to invest as much as they want of the capital gain or proceeds from the sale into a Qualified Opportunity Zone fund. The gain will continue to remain deferred until the earlier of when the QOF is sold or exchanged, or December 31, 2026. There is no limit on the amount of gain that can be deferred in this manner. The additional benefit is that the basis of the new investment in the QOF is stepped up by 10% after 5 years and by 15% after 7 years. If the QOF is held for 10 years, that taxpayer can pay zero capital gains tax on the new investment in the fund.

Overall, the Opportunity Zone Program provides a new and useful opportunity for taxpayers to defer and reduce capital gains. However, research into the actual investment is necessary, as a bad investment with tax benefits is still a bad investment.

This article is intended strictly for educational purposes only and is not a recommendation for or against Qualified Opportunity Funds (QOFs).

Armstrong, Fleming & Moore, Inc. does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Presented by Elizabeth Schleifer