Investing can seem to be a simple concept – buy when the market is low and sell when it’s high – so why is it so tough in practice? There is both a large amount of information available to digest, but also a range of data that is not easily accessible. In short, we can’t possibly know everything. Even when we do get our arms around the situation, we are still human and subject to bias by nature, no matter how small or big that bias may be.

When making a financial decision, it’s important to be aware of what behavioral biases might be influencing us, so that we can find a balance between trusting the behavioral and analytical sides of finance.

AVAILABILITY

The availability bias centers on the type of information that is most easily accessible to us. Often, it surfaces when considering information that we have heard most recently, but it also includes information that is more impactful to us. For example, when the Delta variant became more widespread, did you think about selling your investments to avoid any potential losses? If you lost your job during the beginning of the pandemic, were you fearful that you would lose it again? These are great examples of the availability bias. Even though the situations are different, we can recall our recent memories and determine that there is at least some cause for concern, even if the situation has changed thanks to vaccines and other medical developments.

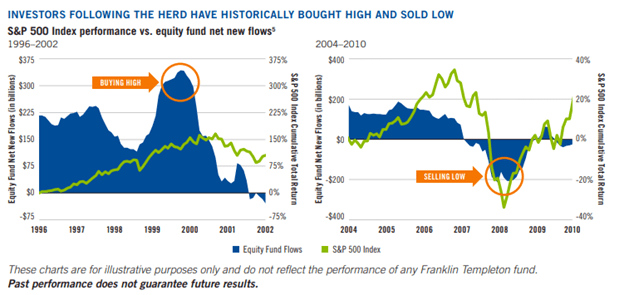

HERDING

As the name implies, the herding bias is all about following the group. It’s a tough bias to overcome: why would we want to be the odd one out and hold our investments while they’re decreasing in value, instead of selling like everyone else? Groupthink is tempting, but often, by the time we decide to join the group, it can be too late. When you’re stuck in traffic and see the lane next to you moving quicker, if you move to that lane is it still moving faster? Or is the lane you were just in now the fast lane? Sometimes you can get to your destination quicker, but other times you would have been better just staying put.

The same principle can be applied to investments: maybe sometimes you will buy/sell at the right time and benefit, but often we find the reverse is true as shown by the graph below. The green line represents the performance of the S&P 500 index, while the blue shaded area represents the volume of purchases and sales of investments. When the blue shaded area is positive, that means people are purchasing more than they are selling and vice versa. When the S&P 500 was near its peak as shown by the graph on the left, that was when investors were purchasing the most and investors sold the most when the S&P was near its lowest value as shown by the graph on the right.

LOSS AVERSION

If presented with the following random chance game, would you play it?

- 75% chance to win $1,000

- 25% chance to lose $500

The odds are in your favor to win, but how many of us would be willing to give up $500 if we lose? What if the amounts are increased?

- 75% chance to win $100,000

- 25% chance to lose $50,000

The odds are still the same, but now the stakes are bigger. $100,000 would make a big impact to many of our lives but stomaching the thought of losing $50,000 is hard to get comfortable with. We can manipulate the numbers so that at some point, each of us would be fearful enough of the loss that we would pass up the opportunity for the gain. This is known as loss aversion.

When considering an investment, we want to determine if the potential benefit will outweigh the risks. If the risks are greater than the benefit, it’s not worth investing. How we weight the risks against the benefits depends on our risk tolerance. For those of us who have a lower risk tolerance, we need more benefit for the same level of risk than someone with a higher tolerance for risk. This can be a particularly challenging bias to overcome as an investor, because taking on risk can help us earn a higher return. But when do you start to lose sleep because of it? When that happens, it might not be worth your while to give up your sanity for the potentially higher return.

PRESENT BIAS

This bias deals with the dilemma between immediate versus long-term needs and wants. If we have the option to receive a reward now or one later, it can be tough to choose the reward later. As you may already be thinking, this bias is very impactful when it comes to saving. If we spend too much now, we may not have enough to meet our needs and wants in the future. But it’s also important to be wary of delaying gratification too much. Ideally, you want to find a balance between delaying rewards to the future and sacrificing your current happiness. We all will likely need to give up something for a future benefit at some point, but we need to decide if it’s worth eating boxed ramen noodles for every meal if we don’t have to.

The four above examples are among the most common biases we experience ourselves and when working with clients. Please reach out to us if you’re interested in learning more.

Presented by Josh Kaplan